The many advantages of Buy Now, Pay Later for retailers

Retailers are always looking for ways to stand out from the competition and payment flexibility could be the latest differentiator. Paradoxically, one area of the payments landscape that is currently seeing a lot of innovation is also one of the oldest – layaways, or “Buy Now, Pay Later” services.

Layaways appeal to customers who want or need to buy something now – maybe an item that is on sale – but don’t carry enough cash and don’t want to use a credit card – or perhaps don’t have one.

Layaways in Openbravo

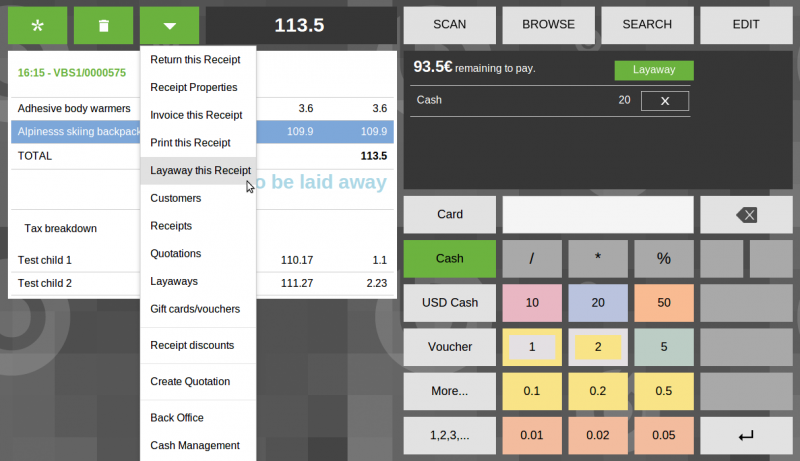

Openbravo Commerce Cloud has offered this capability for some time. With a layaway transaction – see image — the retailer reserves an item for a consumer, who can be named or anonymous, but does not release it until the customer completes all the payments necessary to pay for that item.

The latest variants on the layaway model from Laybuy, Klama and other startups seek to overcome the big disadvantage of traditional layaways, namely that the item is not released to the customer until all payments are completed.

That’s a drawback for shoppers in this era of instant gratification, particularly when shopping online. It also inconveniences the retailer, who must hold the item in the store until full payment is made.

The newer alternatives seek to overcome these drawbacks. For example, with Laybuy’s service, customers must first register on the company’s website and are granted credit based on their credit rating. They can purchase products up to that limit either online or in physical stores, and they receive their purchases immediately, with the payments spread over six weekly installments.

Unlike traditional layaway services, which often charge the customer interest or impose penalty charges for late payment, the new online alternatives do not impose any additional cost on the customer. Instead the retailer pays a commission on each transaction and the BNPL provider is responsible for making all the lending decisions and they assume all liability for repayments.

Layaway as a differentiator

The promoters of these online layaway services say they can be an important differentiation tool for retailers, helping them increase sales, boost conversion rates, and improve average transaction values.

Reducing the friction in the payment process, both in store and online, is an important area for retail innovation. Retailers that want to simplify the buying process and keep their customers happy need to make it easy for customers to use their preferred payment option, whether that be cash, contactless cards, layaways, mobile payments, or new methods that undoubtedly will emerge in the near future.

No Comment